Advisor Movement's Tenure Shift

.avif)

.avif)

.avif)

This is a data-driven midyear review about a shift in advisor movement: the signal is not simply that more advisors are joining firms, but that a larger share of joins are coming from advisors with shorter prior-tenure histories.

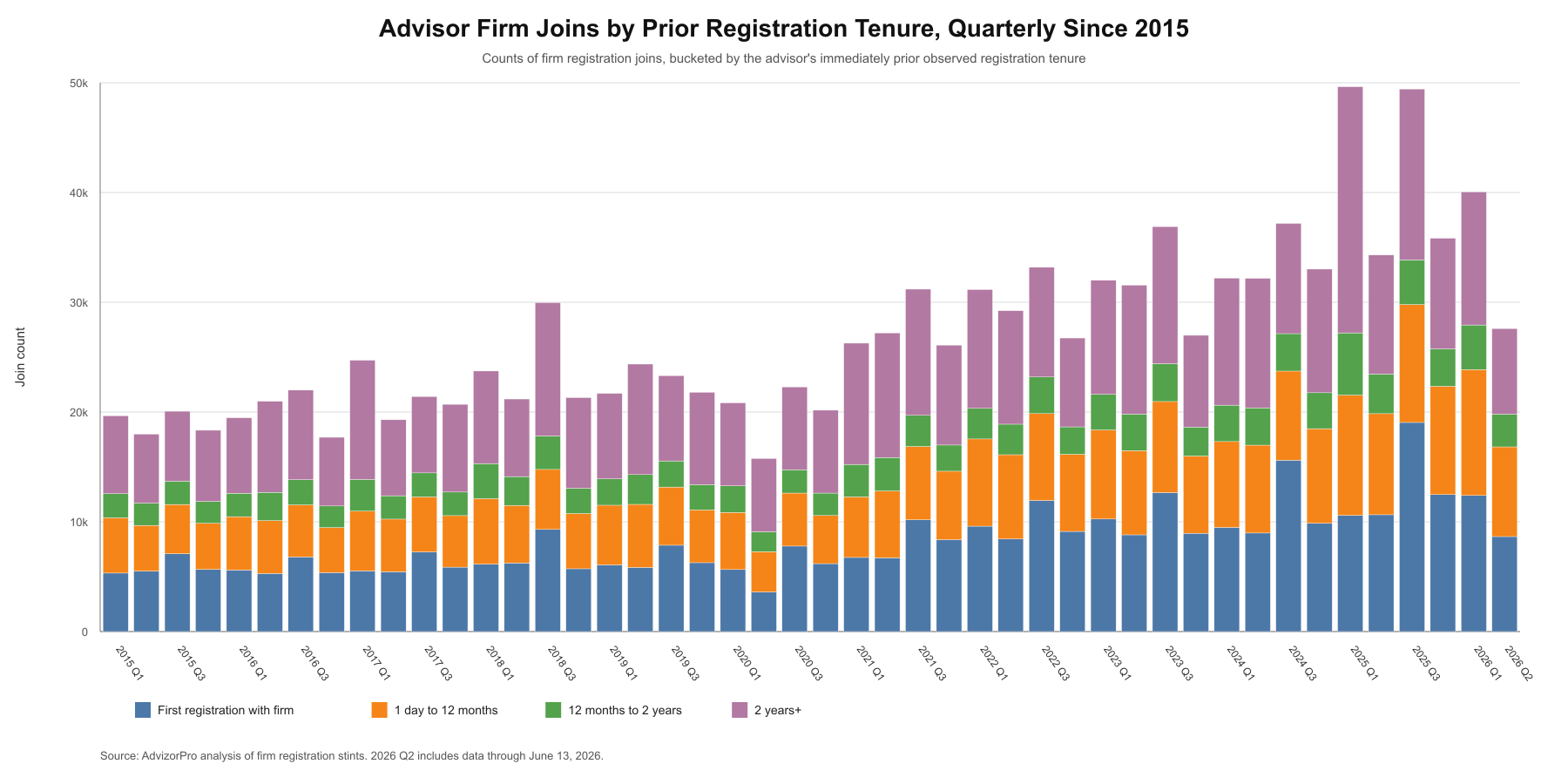

AdvizorPro analyzed quarterly firm-join counts since 2015 and bucketed each join by the advisor's immediately prior observed registration tenure. The clean finding is that first registrations remain relatively stable as a share of total joins, while the 1 day to 12 months prior-tenure bucket has become meaningfully larger in 2026 year to date.

This data:

- Reframes advisor movement around tenure mix rather than anecdotal moves or one-day headlines.

- Is based on a neutral universe of joins, not only selected moves or sub-one-year exits.

- Gives firms a practical midyear question: are recruiting, onboarding, and platform-fit dynamics creating more early-tenure movement?

- Can name firm-level patterns in a follow-on analysis, but the main pitch stands as a market-wide trend piece.

Advisor recruiting headlines often focus on the names, firms, assets and volume of movement. But a midyear review of advisor firm-join data points to a different question: how long are advisors staying in their prior seats before they join the next firm? Our U.S. Wealth Advisor Movement Report found that advisor switching has become the dominant form of movement in the market. This analysis looks one layer deeper, at the tenure mix behind those switches.

That tenure lens changes the story. Looking at quarterly joins since 2015, AdvizorPro grouped each join by the advisor's immediately prior observed registration tenure: first registration with a firm, 1 day to 12 months, 12 months to 2 years, and 2 years plus. The goal was to avoid over-reading a handful of striking moves and instead test whether the broader market mix is changing.

The result is more nuanced than a simple churn narrative. First registrations have not exploded as a share of joins. In 2026 year to date, first registrations account for 31.1% of joins, which is close to the 2015-2019 baseline of 28.9% and the 2025 level of 31.2%.

The sharper shift is in the 1 day to 12 months bucket. From 2015 through 2019, advisors joining after 1 day to 12 months of prior registration represented 23.1% of joins. In 2026 year to date, that share is 29.0%. At the same time, the 2 years plus bucket has declined from 36.9% in the 2015-2019 baseline to 29.4% in 2026 year to date. For context on which firms are capturing the most of this movement, see the latest advisor moves breakdown for May 2026.

In other words, the market is not just producing movement. It appears to be producing a larger share of movement from advisors whose previous registration history was short. That matters because early-tenure movement can point to a different set of firm-level issues than traditional veteran recruiting: onboarding friction, platform mismatch, payout expectations, lead flow, succession uncertainty, compliance constraints, or weak cultural fit.

For wealth management firms, the implication is practical. Recruiting success cannot be measured only by signed advisors or announced moves. A growing short-tenure join mix raises the importance of first-year retention, realistic transition promises, manager involvement after the start date, and early warning indicators that an advisor is not settling in. Understanding which channels advisors are moving from also matters: our advisor channel migration analysis shows that wirehouse advisors remain the most cross-channel mobile, while RIA advisors demonstrate the highest retention once they reach independence.

For advisors, the same data raises a strategic question. More frequent early movement may reflect a more fluid market, but it also makes due diligence more important. Before making a move, advisors need sharper answers on client portability, technology, support staff, compliance review, economics and the lived experience of advisors who joined the firm recently.

The tenure mix is not a complete explanation of advisor mobility. It does not, by itself, identify whether a given move was voluntary, part of a transaction, or driven by firm-level restructuring. But as a midyear market signal, it suggests the industry should watch not only how many advisors are moving, but how quickly they are moving again.

Figure 1. Quarterly joins by prior registration tenure

Source: AdvizorPro analysis. 2026 Q2 includes data through June 13, 2026.

Data snapshot

Methodology note

The analysis counts firm registration joins from 2015 through June 13, 2026. Each join is counted in the quarter of the new firm registration and bucketed by the advisor's immediately prior observed registration tenure. First registration means the first observed registration stint for that advisor in the database.

The analysis is intentionally neutral: it counts joins broadly rather than screening only selected moves or short-tenure exits. Additional reporting would be needed before attributing any specific firm-to-firm pathway to recruiting strategy, M&A, platform conversion, or other transaction activity.

Top firms with increased 0-24 month hiring mix

This table compares each destination firm’s share of joins in the 0-24 month buckets across the recent trailing-four-quarter window (2025 Q3 through 2026 Q2 to date) versus the prior four quarters (2024 Q3 through 2025 Q2). Firms are ranked by percentage-point increase. Minimum: at least 50 joins in both periods; at a 100-join threshold, nine firms qualified.

Firm-level caution: This ranking is a screening list, not proof of purely organic recruiting. Public-source checks suggest Osaic, LPL Enterprise and Empower may include platform, rebrand or transaction-related effects, so those entries should be reported individually before being used as examples of deliberate short-tenure hiring strategy. The remaining names did not show an obvious comparable 2025-2026 conversion signal in a quick public-source check, but firm-level attribution should still be treated cautiously.

About AdvizorPro

AdvizorPro is the advisor intelligence platform built for asset managers, ETF issuers, wealthtechs, and distribution teams that need to identify, prioritize, and engage financial advisors. With verified data across 750,000+ RIAs, family offices, and broker-dealers - combined with AI-powered lead scoring, TrafficIQ visitor intelligence, native CRM integrations, and now direct connectivity to Claude and ChatGPT - AdvizorPro powers the go-to-market strategies of leading firms across the wealth management ecosystem.

Ready to accelerate your advisor distribution strategy? Book a quick demo

Written by: Cole Cummings

Cole Cummings is the Director of Marketing at AdvizorPro and a B2B SaaS marketer with multiple years of experience in the fintech industry. He leads all of AdvizorPro’s data-driven research and industry reports, giving him deep expertise in the RIA ecosystem and the trends shaping advisor behavior, allocation decisions, and firm growth across wealth management.

Related Post

Related insights you may find valuable

.webp)