Advisor Demographics & Team Structures Report 2025

.avif)

.avif)

.avif)

Executive Summary

The U.S. financial advisor landscape is in a state of generational and structural transition. With an aging advisor base, uneven gender representation, and increasing team complexity, firms face mounting pressure to adapt their strategies for recruiting, marketing, and long-term planning.

This report, powered by AdvizorPro’s person-level dataset, analyzes over 776,000 securities-licensed advisors and 44,700 registered firms as of June 1, 2025. It blends SEC ADV filings with proprietary web data, AI-powered entity extraction, and manual research to uncover key trends in advisor age, gender, firm structure, and lifestyle signals across RIAs, broker-dealers, hybrids, family offices, and institutional wealth channels.Key insights include:

- More than 1 in 7 advisors is over age 60, with succession risk especially high in solo RIAs and wirehouses

- The average team remains lean (2.8 advisors), but a long tail of scaled firms is reshaping service models

- Female advisor representation remains below 25% overall, but ownership and executive roles are growing. These dynamics are explored further in our 2025 Advisor Demographics & Team Structures Report Part 2 – Female Leadership, Advisor Diversity & Personal Signals.

- Lifestyle signals such as hobbies show new opportunities for personalization in a relationship-driven industry

This data-driven report equips firms with the context needed to refine distribution, recruiting, and engagement strategies in line with evolving advisor demographics and firm structures.

Table of Contents

- Introduction & Methodology

- Firm Size Definitions

- Part I: Advisor Age Trends & the Coming Succession Wave

- Advisor Age Distribution

- Advisor Age by Channel

- Advisor Age by RIA Firm Size

- Advisors Over Age 60 by Channel

- Geographic Retirement Exposure

- Part II: Advisor Team Structures & the Shift Away from Solo Practices

- Team Size & Composition Trends

- Advisor Team Rankings

- Solo vs. Team-Based Advisor Comparison

- Part III: Diversity Signals & Personal Identifiers in the Advisor Landscape

- Gender Representation

- Gender by Channel

- Gender by Geography

- Female Ownership Snapshot

- Advisor Lifestyle Signals

- About AdvizorPro

Firm Size Definitions

Part I: Advisor Age Trends & the Coming Succession Wave

Succession planning has become a top strategic topic for asset managers, platforms, and RIAs alike. With more than 1 in 7 advisors over age 60, this section explores where retirement risk is most concentrated — and how it varies by firm type, channel, and geography. For many firms, these dynamics also open the door to M&A opportunities, as outlined in our RIA M&A Playbook: How to Evaluate Targets Using Data.

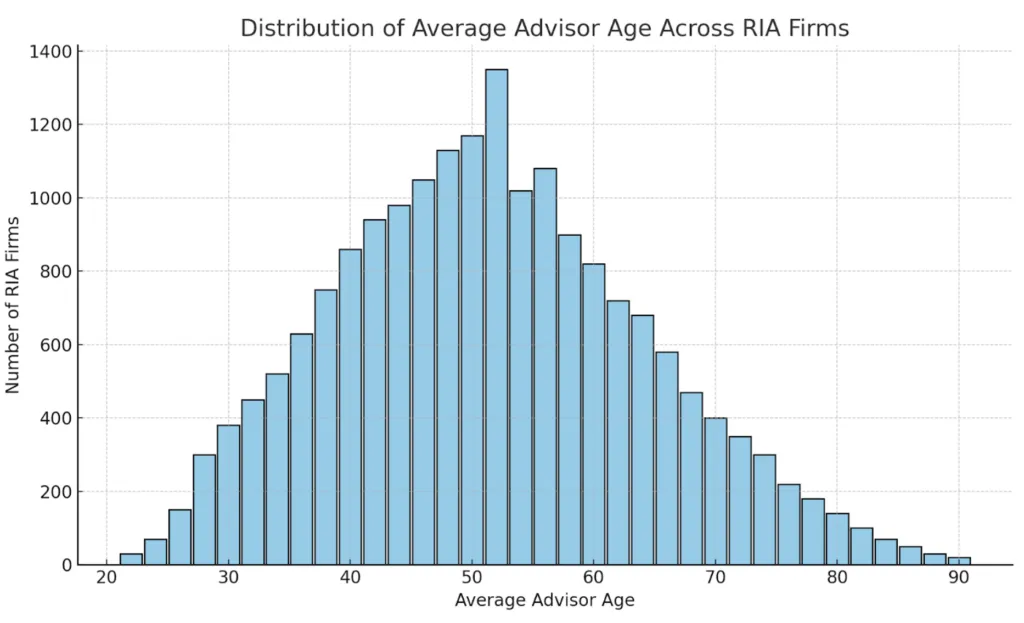

Advisor Age Distribution

The average U.S. advisor is 46.7 years old, with a median age of 46. Notably, 14.4% of advisors are over 60, indicating a significant cohort approaching retirement.

Key Insights: The advisor population is aging, with more professionals in their 50s and 60s than in their 20s and early 30s. While there is a visible pipeline of younger talent — particularly in the 35–45 age range — it may not be sufficient to fully replace retiring advisors, especially in solo practices. This underscores the dual need for succession planning and early-career advisor development.

Advisor Age by Channel

This table highlights how advisor age varies by firm channel, revealing structural and cultural differences across the wealth management landscape.

Key Insights: Wirehouse advisors are the oldest, reflecting legacy structures and a slower pace of independence transitions. RIA and hybrid advisors are significantly younger and more growth-oriented. IBDs land in the middle, reflecting a range of affiliations and transition timelines.

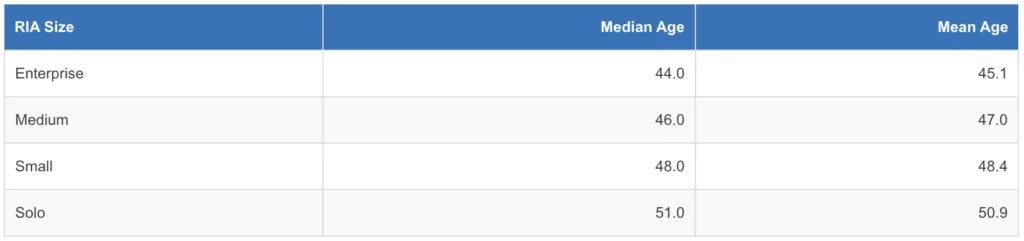

Advisor Age by RIA Firm Size

Advisor age also varies widely depending on firm size and structure.

Key Insights: Solo RIAs are significantly older than enterprise firms, highlighting succession opportunities and book acquisition potential.

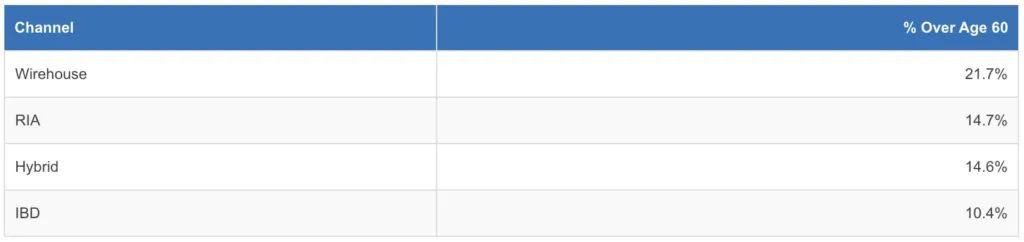

Advisors Over Age 60 by Channel

This view identifies which channels face the greatest concentration of advisors above traditional retirement age.

Key Insights: Wirehouses have the highest near-term succession risk.

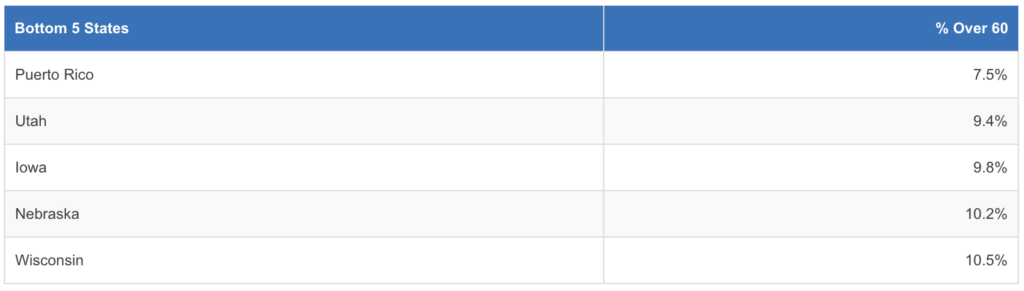

Geographic Retirement Exposure

Certain regions face outsized exposure to aging advisor populations.

Key Insights:

- Succession exposure is regionally affected.There's a nearly 3x difference between the states with the highest and lowest share of advisors over 60.

- Younger advisor populations suggest growth potential for fintechs, recruiters, and RIAs building for the long term.

- Aging-in-place is common; many older advisors are delaying exits.

Part II: Advisor Team Structures & the Shift Away from Solo Practices

This section explores how advisor practices are structured—from solo shops nearing retirement to scaled teams driving growth. These structural differences shape decision-making dynamics, operational complexity, and partnership potential.

Team Size & Composition Trends

The mean advisor team size is 2.8 advisors, and the median is 2, confirming that most teams remain relatively lean. The distribution of team sizes shows a sharp drop-off after the smallest structures, with one- and two-person teams making up the bulk of the advisor landscape.

While smaller teams dominate numerically, a growing cohort of larger, high-scale teams, though fewer in number, represent the operational future of the industry. These teams frequently centralize investment decisions, build multi-role staffing models, and adopt outsourced planning or investment platforms to drive efficiency.

Within this distribution, RIA firms report an average advisor age under 40, accounting for 21.1% of all team-based RIAs analyzed. These younger teams tend to be more tech-forward, process-driven, and growth-oriented.

They are also more likely to engage with digital tools, explore OCIO or TAMP partnerships, and scale through operational leverage rather than headcount alone.

Key Insight: While the typical advisor team remains small, the rise of scaled, younger, tech-enabled teams signals a shift in how practices grow. This long tail of high-complexity firms represents a disproportionate share of influence, growth momentum, and platform demand.

Advisor Team Rankings

Advisor team structures vary widely across firms and channels - shaped by legacy business models, recruiting strategy, and how each firm approaches growth. Some prioritize team depth through large, integrated advisor groups. Others focus on team breadth, supporting thousands of smaller teams spread across decentralized networks.

Top Firms by Total Advisor Teams

These firms lead the industry in total number of mapped advisor teams:

- Merrill Lynch

- Morgan Stanley

- LPL Financial

- Osaic Wealth

- UBS Financial Services

- RBC Capital Markets

- Cambridge Investment Research

- Stifel Nicolaus

- Northwestern Mutual

- MML Investors Services

These rankings reflect verified team relationships among licensed advisors, not inflated branch affiliations or roll-up structures.

Merrill Lynch and Morgan Stanley top the list due to the scale and maturity of their team-based models, many of which operate as institutional-style units with long-established client rosters. In contrast, firms like LPL and Osaic leverage large OSJ networks and an IBD-style footprint, supporting thousands of semi-autonomous advisor groups across the country.

Wealth Management Firms with ≥50 Teams, Ranked by Average Team Size

Firms like Mariner Wealth and Equitable Advisors have aggressively built high-density teams, often through acquisitions, tuck-ins, or career-pathing programs that reward team integration.

Mariner’s team structures, for example, often include specialists in planning, investments, and business operations—reflecting the firm’s evolution into a full-scale wealth enterprise.Meanwhile, Merrill Lynch maintains a vast number of teams but with smaller average size, signaling its “scale through breadth” model.

Despite modest team size, Merrill’s high multi-advisor rate (80.1%) points to a culture of collaboration and centralized service models—especially in key metro markets.

Key Insight:Some firms scale through depth, building larger, more centralized advisor teams that mirror institutional investment desks. Others scale through breadth, supporting vast networks of smaller teams that operate with autonomy.

These structural choices shape how firms staff, sell, adopt new tools, and make investment decisions—critical context for product providers, recruiters, and integration partners.

Solo vs. Team-Based Advisor Age, Gender, & Tenure Comparison

Solo advisors and team-based advisors represent two fundamentally different models of practice and two distinct phases in the advisor lifecycle. The data below highlights key demographic and experiential differences between the two groups and highlights how solo advisors differ from their team-based peers in terms of age, gender, and experience.

Conclusion: Preparing for the Next Era of Financial Advisors

The U.S. advisor landscape is undergoing a profound generational and structural shift. With succession pressures mounting, team-based models rising, and diversity slowly improving, the firms that succeed will be those that adapt early, building strategies around data-driven recruiting, smarter segmentation, and personalized engagement.

AdvizorPro equips asset managers, platforms, and fintechs with the advisor-level intelligence needed to navigate these changes, turning demographic and structural trends into actionable opportunities.

If you are ready to refine your recruiting and distribution strategies with data built for today’s advisor landscape, Start your free trial and see how AdvizorPro can power your growth.

Written by: Cole Cummings

Cole Cummings is the Director of Marketing at AdvizorPro and a B2B SaaS marketer with multiple years of experience in the fintech industry. He leads all of AdvizorPro’s data-driven research and industry reports, giving him deep expertise in the RIA ecosystem and the trends shaping advisor behavior, allocation decisions, and firm growth across wealth management.

Related Post

Related insights you may find valuable

.webp)