Find and Win More RIA & Family Office Clients

Built on Verified Data + Advanced AI Intelligence

- 750,000+ Verified RIA and Family Office profiles

- Search and filter by AUM, custodian, and specialization

- The smarter, faster alternative to outdated advisor databases

Everything You Need to Win the Right Clients

Find Your Prospects

Filter by AUM, platform, ETF holdings, lead score, and more. Your entire market, on demand.

Trust Your Data

Verified contacts, accurate AUM, up-to-date data. Built for teams that can't afford bad data.

Win Your Meeting

See their holdings, recent changes, tech stack, and key contacts before you ever reach out.

AdvizorPro was Built For:

.svg)

Connect AdvizorPro to Your AI Tools

Connect the industry's most accurate advisor intelligence directly to the AI tools you're already using.

Our AI connection lets you bring real-time RIA and advisor data into your AI workflows — no exports, no stale spreadsheets, no switching tabs. Ask questions in plain English and get answers pulled directly from AdvizorPro's verified dataset, right inside Claude, ChatGPT, or your internal AI tools.

Learn MoreFeatures

CRM integration

Sync seamlessly with Salesforce, HubSpot, and Dynamics auto-enrich contacts, push smart lists, and power real-time workflows.

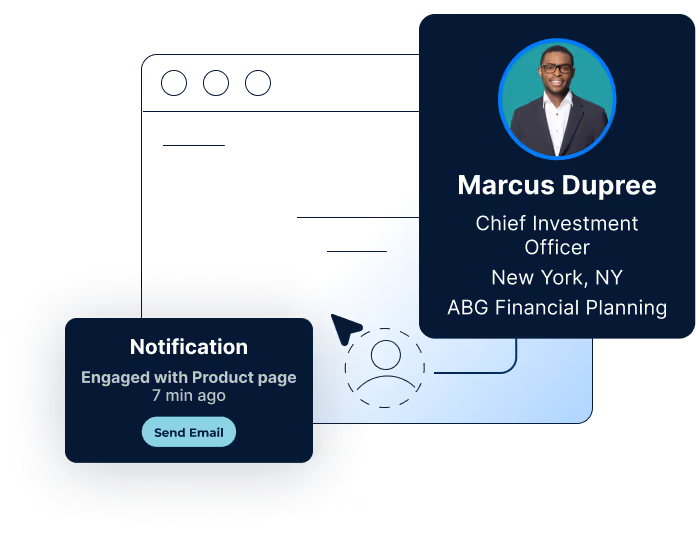

Traffic IQ

Know which RIAs are on your site even before they fill out a form. Turn anonymous traffic into outreach-ready insights that power sales and marketing workflows.

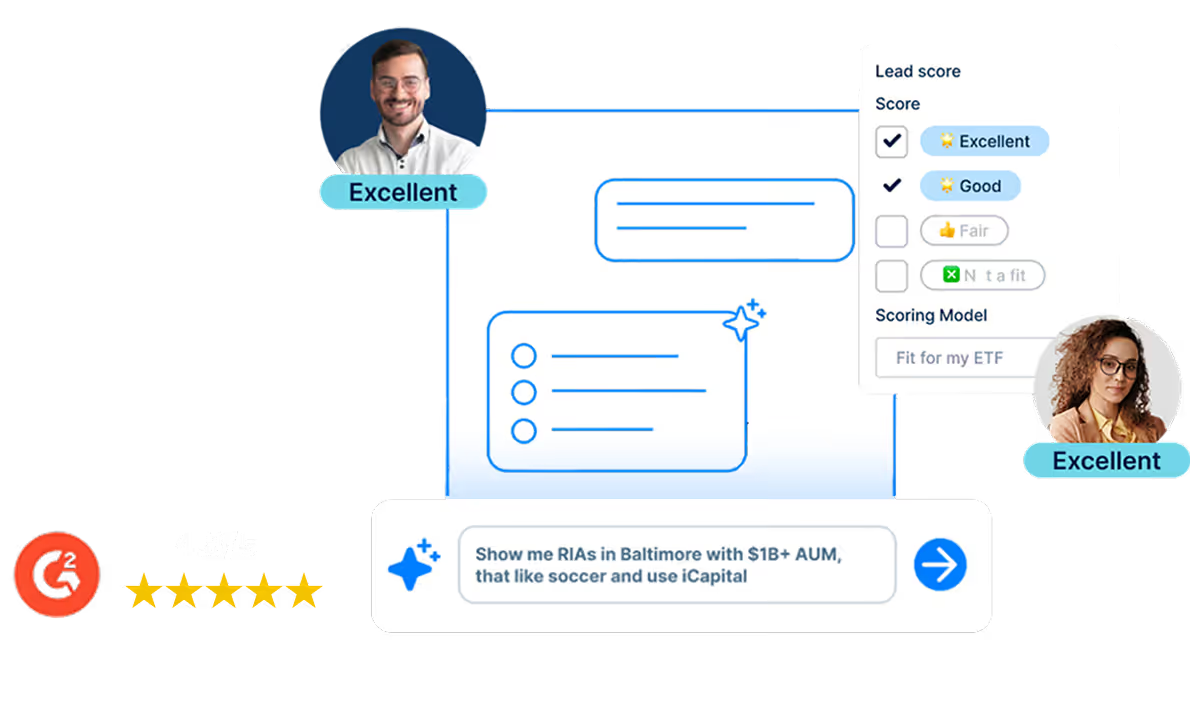

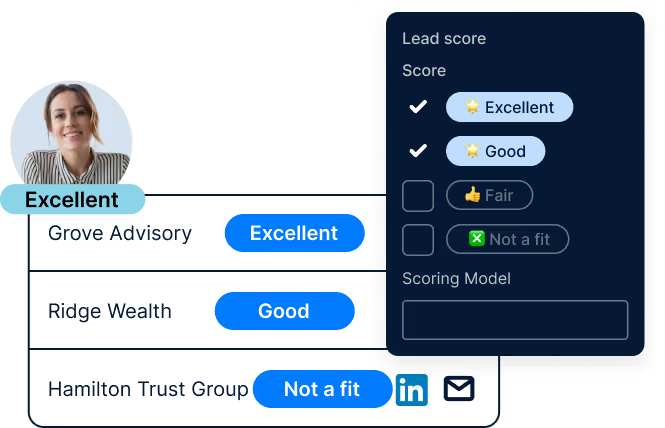

Lead Scoring

Automatically score advisors and firms using location, AUM, custodian, keyword tags, and site visit activity to prioritize best-fit leads.

Tech Stack

See which firms use tools like Orion, Envestnet, or eMoney - ideal for wealthtechs identifying RIAs using competitors or asset managers targeting specific platforms.

Contact Intelligence

Reach decision-makers across RIAs, family offices, and more with verified titles, emails, and phone numbers at scale.

AI Search Assistant

Chat with our in-app AI assistant to run searches using plain English. It builds queries and filters directly in the platform.

Wealth Team Intel

Navigate complex orgs at wirehouses, banks, and large IBDs. With over 25,000 teams mapped, see structure, key contacts, and reporting lines reach the right leaders, not just a name.

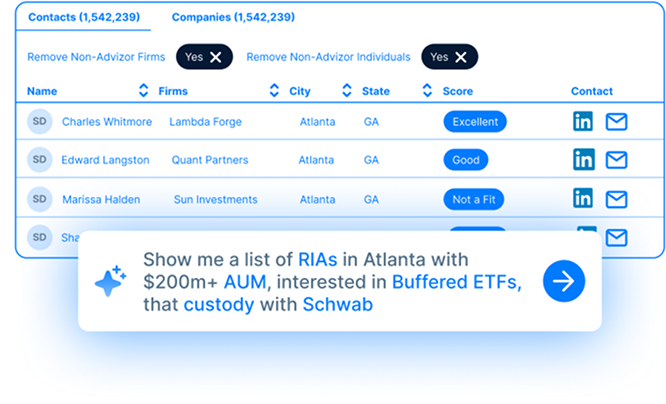

List Matching

Upload advisor lists from conferences, webinars, or inbound leads, and match them to enriched profiles with firm data, contact info, scoring, and CRM-ready exports.

.png)

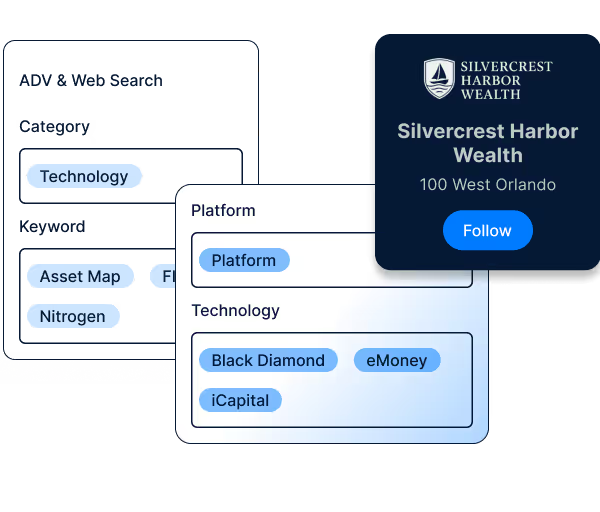

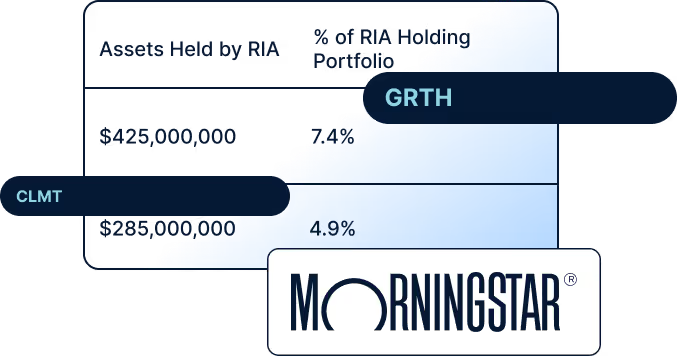

ETF Holdings

See which RIAs hold your competitors’ ETFs or others in the same Morningstar category great for identifying prospects or tracking demand shifts.

How AdvizorPro Turns

RIA Prospects into Clients

Target High-Value RIAs

Our AI surfaces wealth advisors and family offices actually in the market - based on behavior, product interest, and contact/firm-level intent signals. It's smarter targeting, not guesswork.

Turn Website Traffic Into Pipeline

Identify anonymous RIA and family office visitors and push them directly into your workflows-turning passive traffic into warm, high-intent leads your sales and marketing teams can act on immediately.

Activate Your CRM

Turn your CRM into a growth engine. Sync verified advisor data, automate enrichment, and push fresh insights into every field - so your sales and marketing teams act on accurate, up-to-date intelligence every day.

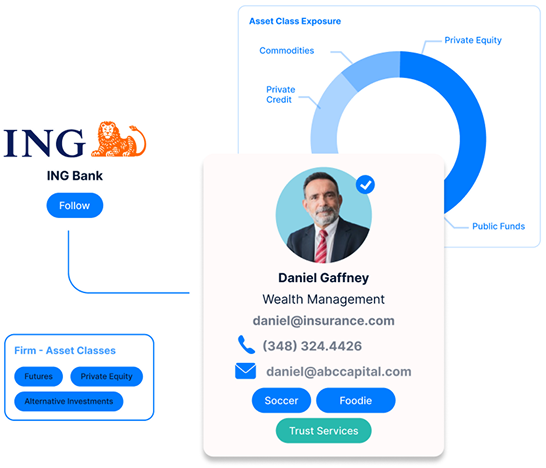

Get Inside the Advisor Mindset

Whether it's ETF holdings, tech stack, TAMP affiliation, hobbies, team structure, or niche focus areas we surface the intel that helps you personalize every message, meeting, and move.

Testimonials

“The team from AdvizorPro could not be more helpful. Not only do they provide great training both directly and via video tutorials, but they are also available for one-off questions at a moment's notice. Super knowledgeable and super responsive!”

"A big round of applause to your entire team; I’m glad to have you as our partner!"

"AdvizorPro runs circles around the competition."

“AdvizorPro has been a tremendous addition to our sales operations, delivering real, industry-specific data and support that feels like a true partnership.”

“We evaluated a few options, before landing on AdvizorPro, and we're really glad we did. The data quality is better, the CRM integration has completely transformed how we enrich and manage our contacts, and the AI insights have made our team way more efficient. But honestly, what's stood out most is the partnership. They've been genuinely invested in our success from day one. We're growing, and we couldn’t be happier.”

“It’s rare to find a partner with both robust data and amazing service, AdvizorPro delivers both. Turning data headaches into actionable insight.”

“It is not often that I am wowed by a vendor, but the team over at AdvizorPro goes above and beyond. The service level is unmatched and their product has been an integral part of our sales process from day 1 of our relationship."

View Recent Blog Posts

News, strategies, and real-world examples from across the wealth management and family office industry.

.avif)

.avif)

Stop wasting time searching.

Start building relationships with the right wealth advisors & family offices

Book A Quick Demo